Stone Mountain Corporation

Re$erve Studies

Stone Mountain Corporation

Re$erve Studies

The following California Civil Codes apply to Reserve Studies for community associations:

Civil Code §5550 -- Reserve Study Requirements

Civil Code §5560 -- Reserve Funding Plan

Civil Code §5565 -- Summary of Association Reserves

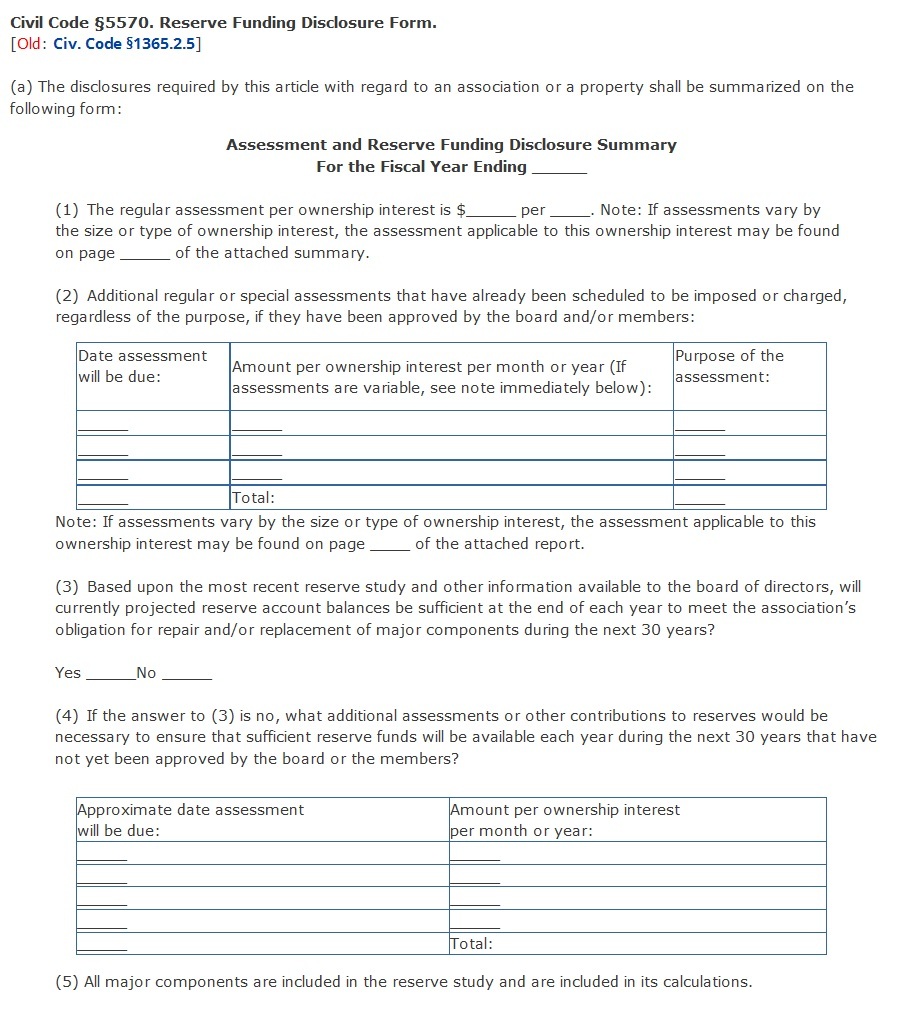

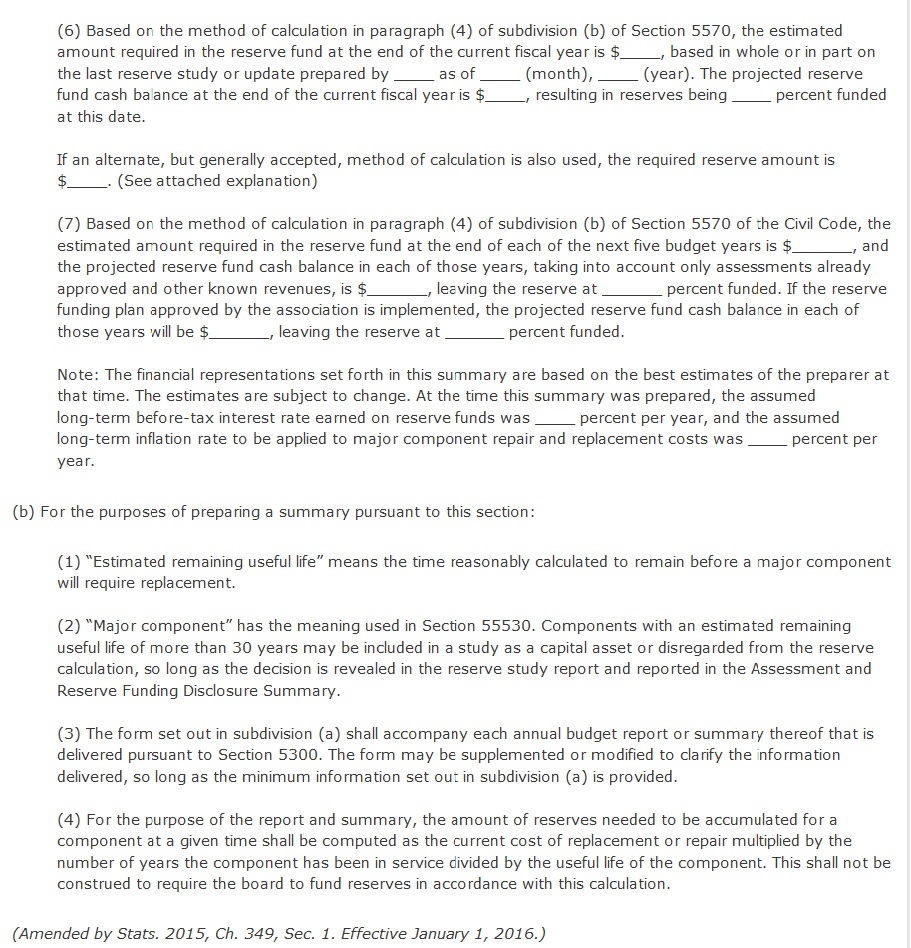

Civil Code §5570 -- Reserve Funding Disclosure Form

Each of the above Civil Code sections are listed here, but please be aware that the State Legislature revises the wording of these Civil Code sections periodically, so the text listed below is current as of January 1, 2017. Before relying on the information presented herein, you should check the most recent Civil Code. The www.davis-stirling.com website is often considered to be the best online source for up-to-date Civil Code.

There are three primary reasons for your association to abide by these laws:

The rationale behind these rules is to ensure that community associations adopt sound financial practices to save reserve funds for long-term capital expenses, and

Proper disclosure of the financial status of community associations is essential for financial transparency. Reserve Funding disclosures must be sent to all members of an association. And new buyers and lenders often ask to see the Reserve Study and the Reserve Disclosures before a home is sold in an association.

Even though the State doesn’t seem to have the resources to enforce the numerous Civil Codes they apply to homeowners associations, there is an incentive to abide by them because if there is future litigation against the HOA or the Board in the future, the Board and HOA can be vulnerable to claims of failure to follow essential Civil Code financial practices.

Civil Code §5550 -- Reserve Study Requirements

"http://www.davis-stirling.com/MainIndex/Statutes/CivilCode5550/tabid/3816/Default.aspx#axzz2CgHrcBrn"

Civil Code §5550(a) At least once every three years, the board shall cause to be conducted a reasonably competent and diligent visual inspection of the accessible areas of the major components that the association is obligated to repair, replace, restore, or maintain as part of a study of the reserve account requirements of the common interest development, if the current replacement value of the major components is equal to or greater than one-half of the gross budget of the association, excluding the association’s reserve account for that period. The board shall review this study, or cause it to be reviewed, annually and shall consider and implement necessary adjustments to the board’s analysis of the reserve account requirements as a result of that review.

(b) The study required by this section shall at a minimum include:

1) Identification of the major components that the association is obligated to repair, replace, restore, or maintain that, as of the date of the study, have a remaining useful life of less than 30 years.

(2) Identification of the probable remaining useful life of the components identified in paragraph (1) as of the date of the study.

(3) An estimate of the cost of repair, replacement, restoration, or maintenance of the components identified in paragraph (1).

(4) An estimate of the total annual contribution necessary to defray the cost to repair, replace, restore, or maintain the components identified in paragraph (1) during and at the end of their useful life, after subtracting total reserve funds as of the date of the study.

(5) A reserve funding plan that indicates how the association plans to fund the contribution identified in paragraph (4) to meet the association’s obligation for the repair and replacement of all major components with an expected remaining life of 30 years or less, not including those components that the board has determined will not be replaced or repaired.

(Added by Stats. 2012, Ch. 180, Sec. 2. Effective January 1, 2013. Operative January 1, 2014, by Sec. 3 of Ch. 180.)

Civil Code §5560 -- Reserve Funding Plan

"http://www.davis-stirling.com/MainIndex/Statutes/CivilCode5560/tabid/3817/Default.aspx#axzz2CgHrcBrn"

Civil Code§5560(a) The reserve funding plan required by Section 5550 shall include a schedule of the date and amount of any change in regular or special assessments that would be needed to sufficiently fund the reserve funding plan.

(b) The plan shall be adopted by the board at an open meeting before the membership of the association as described in Article 2 (commencing with Section 4900) of Chapter 6.

(c) If the board determines that an assessment increase is necessary to fund the reserve funding plan, any increase shall be approved in a separate action of the board that is consistent with the procedure described in Section 5605.

(Added by Stats. 2012, Ch. 180, Sec. 2. Effective January 1, 2013. Operative January 1, 2014, by Sec. 3 of Ch. 180.)

Civil Code §5565 -- Summary of Association Reserves

"http://www.davis-stirling.com/MainIndex/Statutes/CivilCode5565/tabid/3818/Default.aspx"

Civil Code§5565 - The summary of the association’s reserves required by paragraph (2) of subdivision (b) of Section 5300 shall be based on the most recent review or study conducted pursuant to Section 5550, shall be based only on assets held in cash or cash equivalents, shall be printed in boldface type, and shall include all of the following:

(a) The current estimated replacement cost, estimated remaining life, and estimated useful life of each major component.

(b) As of the end of the fiscal year for which the study is prepared:

(1) The current estimate of the amount of cash reserves necessary to repair, replace, restore, or maintain the major components.

(2) The current amount of accumulated cash reserves actually set aside to repair, replace, restore, or maintain major components.

(3) If applicable, the amount of funds received from either a compensatory damage award or settlement to an association from any person for injuries to property, real or personal, arising out of any construction or design defects, and the expenditure or disposition of funds, including the amounts expended for the direct and indirect costs of repair of construction or design defects. These amounts shall be reported at the end of the fiscal year for which the study is prepared as separate line items under cash reserves pursuant to paragraph (2). Instead of complying with the requirements set forth in this paragraph, an association that is obligated to issue a review of its financial statement pursuant to Section 5305 may include in the review a statement containing all of the information required by this paragraph.

(c) The percentage that the amount determined for purposes of paragraph (2) of subdivision (b) equals the amount determined for purposes of paragraph (1) of subdivision (b).

(d) The current deficiency in reserve funding expressed on a per unit basis. The figure shall be calculated by subtracting the amount determined for purposes of paragraph (2) of subdivision (b) from the amount determined for purposes of paragraph (1) of subdivision (b) and then dividing the result by the number of separate interests within the association, except that if assessments vary by the size or type of ownership interest, then the association shall calculate the current deficiency in a manner that reflects the variation.

Civil Code §5570 -- Reserve Funding Disclosure Form

"http://www.davis-stirling.com/MainIndex/Statutes/CivilCode5570/tabid/3819/Default.aspx"

To help clients understand the nuances of the foregoing “Assessment & Reserve Disclosure Form”, Chris Andrews wrote two articles in 2005 and 2007 which explain everything in detail.

1...THE “ASSESSMENT AND RESERVE FUNDING DISCLOSURE SUMMARY“– Demystified…

2...The 2007 Revisions to the Required Reserve Disclosure

Return To Top